Global chip shortage: Mitigating its impact on consumer electronics

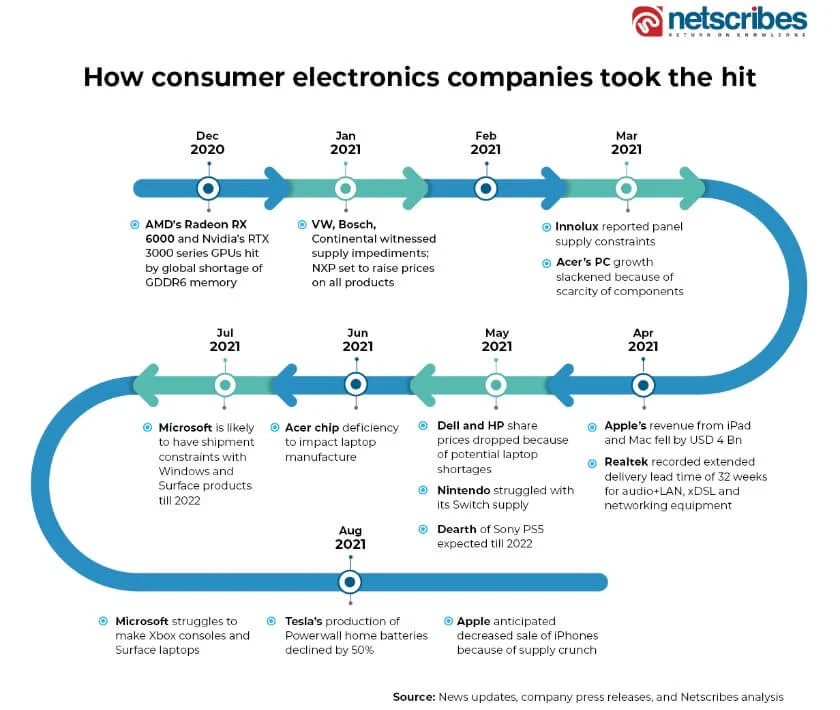

In September this year, the time gap between companies placing orders for semiconductor chips and receiving them hit an all-time high: 21 weeks. In one such instance, the chip supply chain disruption has cost consumer electronics giant Apple USD 6 billion.

The global chip shortage has halted the production of consumer electronics worldwide. In turn, this has sent manufacturers, product companies, and end consumers into a frenzy. Equipment manufacturers have started to play catch-up in the volatile consumer technology market. The ongoing global chip shortage crisis, however, will likely last through 2023. So, companies need to proactively take steps to navigate the same and to prevent similar setbacks in the future.

Decoding the cause

In recent years, there has been a constant demand for edge devices. Moreover, the proliferation of digital technologies such as AI, cloud, IoT, Industry 4.0, robotics, and autonomous driving have further increased the global demand for semiconductor chips. If this wasn’t enough, COVID-19 accelerated companies’ digital transformation initiatives, cutting short years of planned investment. Given this, consumer electronics manufacturers found themselves at the mercy of chip fabrication companies to cater to the growing enterprise appetite for remote working equipment in the form of PCs, joysticks, gaming consoles, laptops, cloud storage, and webcams.

In short, the global chip shortage of 2020-21 is a result of several external factors. These include the COVID-19 outbreak, acceleration of digitization, rising trade tensions in the U.S. and China, the traditional “just-in-time” component inventory model followed by OEMs globally, and rapidly changing consumer habits. Furthermore, even natural disasters such as Japan’s 7.3-magnitude earthquake in February this year forced chip plants to shut down.

Read more: The impact of COVID-19 on China’s manufacturing industry

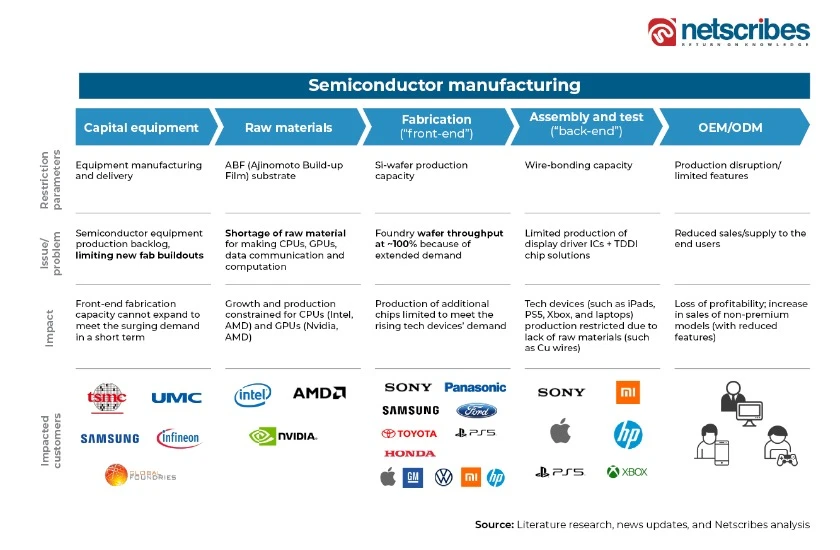

Current bottlenecks in the chip supply chain and its impact on consumer electronics

According to Netscribes analysis, lead times for semiconductor value chain expansion may take up to three years. This translates into the ecosystem achieving stability by late 2023 or early 2024. The value chain is riddled with bottlenecks such as limited fab buildout, shortage of raw material, wafer throughput at nearly 100%, and OEM disruption due to limited supply to end-users. This has resulted in increased resolution timelines.

If we look at the short-term impact, the front-end fabrication capacity cannot expand to meet the surging demand. Additionally, there is no linear growth and production for CPUs and GPUs. Production of additional chips is limited as compared to the rising demand for tech devices (iPads, PS5, Xbox, and laptops.) This restriction is due to a lack of raw materials (such as Cu wires). The result is a significant drop in profitability.

How can the consumer electronics industry respond to the crisis?

The global chip shortage crisis, now affecting over 160 industries, may continue to negatively impact consumer electronics availability this holiday season. In response, several leading component makers have ramped up their production to mitigate the impact. Here are some insightful strategies and recommendations that can help industry players navigate the upheaval to meet consumer demands.

Read more: Supply chain crisis in consumer electronics and strategies to overcome them

1. Expansion of fab capacity

Two foundries in East Asia – Taiwan’s TSMC and South Korea’s Samsung – manufacture as much as 70% of the world’s semiconductors. TSMC has indicated an investment of USD 100 billion to bolster production. Meanwhile, Samsung plans to spend around USD 205 billion over the next three years to expand fab capacity. Furthermore, Intel claims investment of USD 95 billion to develop new chip facilities in Europe.

Diversification of global manufacturing and expanding fabrication capabilities is one solution that semiconductor companies can explore soon. Most of the shortage is coming from manufacturing line capacity with maxed-out components like power management chips. These chips are manufactured in pretty obsolete plants and use older manufacturing equipment. Increasing the capacity and modernizing the technology here is also a critical part of the solution. This also includes better design portability and making second sourcing part of the design workflow for every new chip design.

According to Saurabh Gupta, Research and Strategy Manager – Semiconductors at Netscribes:

“There is a cascading effect about to set in. With a huge influx of investments to increase the fab capacities and expansion plans, there is a long time to go before the returns start coming back in. This means, increase in prices of the finished product at every node by around 15% and above. Furthermore, it will make the end customers shell out ~20-25% more from their pockets to purchase the same products with same features and specifications.”

2. Rethinking government policies and measures

The proposed initiatives and actions undertaken by various national governments are aimed at strengthening their position in the semiconductor value chain. This can also help increase self-reliance and create better opportunities for international collaborations.

For instance, in South Korea, Samsung and SK Hynix are investing USD 451 billion in chip production for 10 years. The government will provide tax breaks and incentives for chip businesses. It will further encourage funding for the training of 36,000 new staff and other R&D measures. Meanwhile, to respond to China’s competitive threat, the US government has introduced the Facilitating American-Built Semiconductors (FABS) Act. This act will establish an investment tax credit for semiconductor manufacturing in the US. They are also initiating semiconductor-focused dialogues with Japan and South Korea, and establishing the Trade and Technology Council with the EU.

3. Timely response to market changes with the help of predictive insights

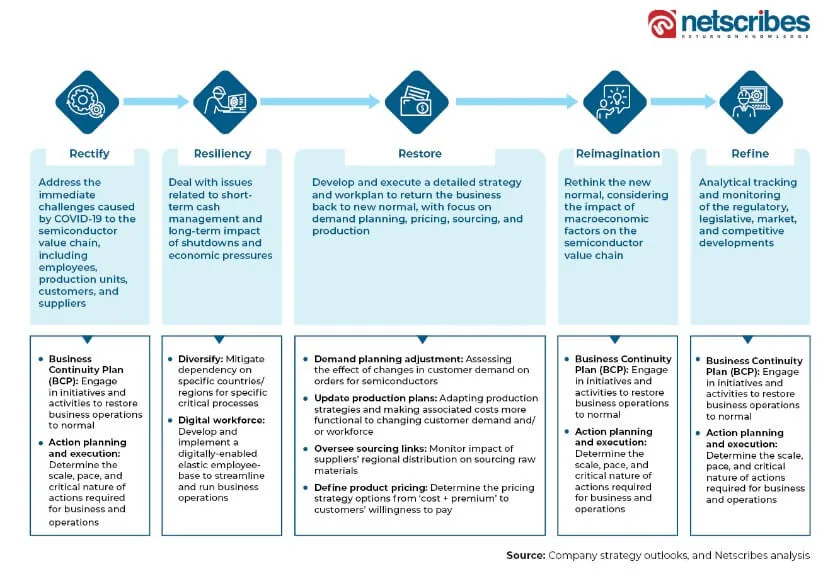

For companies to navigate such a disruption, developing the right blend of predictive insights and analytics capabilities is necessary. This can help to respond to the crisis quickly and effectively while also maximizing impacts across the operating strategy. According to our analysis, companies looking to overcome the global chip shortage crisis should take the following steps.

- Enhance visibility and traceability across the supply chain. Understand tier II/III supply chain and gather continuous market research on critical value chain nodes, and players.

- Conduct real-time market monitoring to identify bottlenecks. Observe the flow of components across the value chain and track lead times, prices, inflations, and deviations, if any.

- Backup supplier network to enable agility. Keep a backup of multiple qualified suppliers ready just in case a risk mitigation strategy is required.

- Collaborative supply planning. Ensure longer-term forecasting (at least for 12 months or so), synchronize customer orders across the value chain, and prepare multi-stage inventory for striking balance between supply and demand.

4. A 5-phase strategy to prevent further chip shortage crisis

Based on our in-house market research expertise, we’ve put together a whitepaper to give you an overview of what the semiconductor chip shortage means for industries and where this crisis is headed. To learn more, please click here.

Industry leaders need to streamline and reevaluate their company strategies to ensure sustained growth and avoid re-entry into similar situations in the future. Maintaining business continuity plans, adjusting demand planning in real-time, tracking competitive dynamics, updating product pricing, and assessing trade environments are all part of the job.

Netscribes market research solution helps you solve your most pressing business challenges – from recognizing growth opportunities and competitive threats to staying future-ready. To learn how you can get a holistic and more accurate view of the market, get in touch with us.